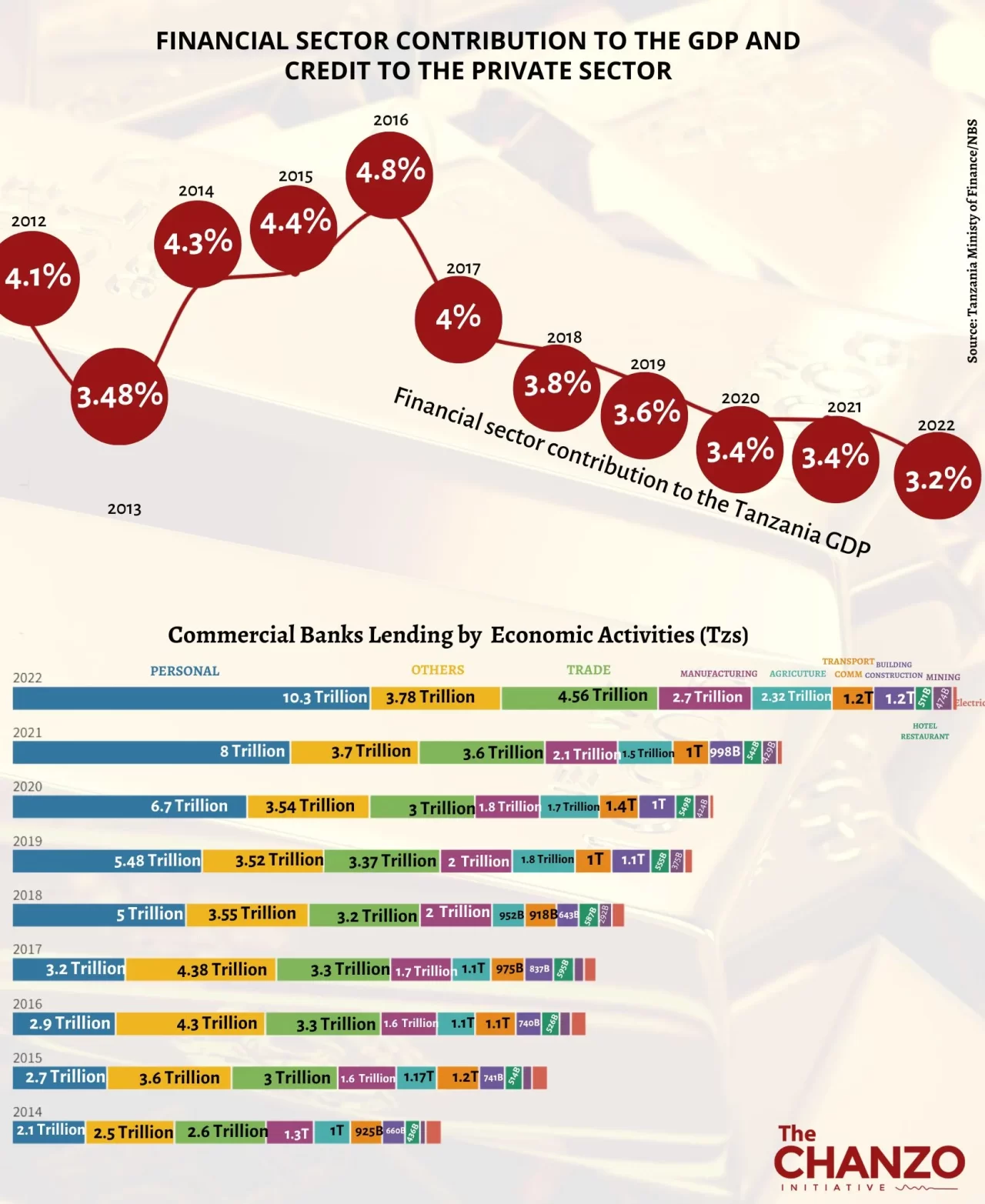

Dar es Salaam. Tanzania’s bankers are having trouble figuring out how to increase their contribution to the economy, reaching the goal of at least ten per cent of the gross domestic product (GDP), a goal that has become distant despite bank growth and windfall profits.

While total bank assets are about 28 per cent of the total GDP, the current contribution of the Tanzanian banks to the economy is about 3.2 per cent of the GDP at the current price, which has been declining over the years.

Reflecting on this situation, Chief Executive Officer of the Tanzania Commercial Bank Adam Mihayo says this is because the banks have not been directing credit to productive sectors of the economy.

“When you look at the contribution of the banking sector to economic growth, it was very minimal, less than five per cent. This has made us think deeply,” said Mr Mihayo during the national tax conference on February 28, 2024, at the Julius Nyerere International Conference Centre (JNICC), in Dar es Salaam.

“One observation is that a large portion of loans issued are personal loans, especially for employees in formal employment,” he added. More than thirty per cent of these loans have gone to individuals.”

Mr Mihayo said banks are yet to direct their investments towards productive sectors of the economy, adding: “We are more than fifty-five banks, and we are all targeting government employees, which is also a limited sector in terms of numbers, if we are all targeting those three million individuals, it can easily reach a point of saturation.”

Data from the Bank of Tanzania (BoT) shows that personal loans have been the largest recipient of bank financing, accounting for about 40 per cent of all loans issued in 2023.

Abdulmajid Mussa Nsekela, CEO of CRDB Bank, Tanzania’s leading bank by assets and second-most profitable bank, believes that circumstances have pushed banks to act this way, starting with COVID-19 and the informality of the economy.

READ MORE: Infographic: Largest Banks in Tanzania 2024

“Let’s not forget historical details,” Mr Nsekela said during the conference. We had COVID-19, which led to the halting of many business operations; it was only workers who were earning something.”

“The majority of businesses in Tanzania are still operating in the informal sector,” he added. We need to make some of the systems more accessible, and people need to be made aware. Loans to the private sector have increased but not to the productive sectors. There is still a need to improve policies that support SMEs.”

Solutions

One problem mentioned as an impediment to contributing to the economy is the availability of enough capital to provide loans to various sectors.

READ MORE: Infographic: Banks And Mobile Networks In Tanzania Have Issued Loans Amounting To 50.9 Trillion

Kamal Quadir, Founder and CEO of bKash, a digital financial service that serves about 70 million banked, underbanked, and unbanked people in Bangladesh, believes the solution lies in technological innovation that reflects the actual environment.

“It’s widespread for middle-class and rich people to save and that saving pool to be used to enrich various sectors of the economy,” Mr Quadir said during the recently concluded 21st Conference of Financial Institutions (COFI) on March 08, 2023, at the Arusha International Conference Centre (AICC).

“But technology has allowed impoverished people to participate in capital pool creation, that capital pool is maintained in a trust account, and that capital can then be used for social and economic development,” he added.

Other experts believe that the capital pool can be increased if people migrate to using more digital solutions for sending and receiving money and buying and selling.

Firas Ahmad, CEO of AzamPay, highlighted this question in his response to Quadir’s presentation: “How do you move from a system based on money movement into a system based on commerce facilitation?”

One of the impediments mentioned during the discussion is the cost of using digital systems, which experts believe is the current roadblock in ensuring that more of the population uses digital tools.

Prof Esther Ishengoma, one of Tanzania’s respected financial researchers, thinks that the issue with broader adoption is cost, which she calls “very important.”

“There was a day I wanted to buy something, and I didn’t have enough cash, so I decided to use Lipa Namba,” she recounted. “Sh3,000 was charged for just one transaction. But If I withdraw Sh400,000 at a lesser cost, I can meet all my transactions.”

“If I, the [university] professor, am using cash, what do you expect from people in the villages?” asked Ishengoma, who was also a panellist at the conference.

Emphasising this point, Muhsin Masoud, the Managing Director of the People’s Bank of Zanzibar (PBZ), said: “Sometimes customers see that if they withdraw their money and do a transaction using cash, it is cheaper than using digital means. That is the key issue; we need to look at the cost.”

READ MORE: Development From Below? This Is the Story of a Daladala Co-op in Dar es Salaam

Another proposed solution to ensuring banks have enough liquidity to contribute more to the economy is for the government to set a policy environment that can support banks.

“Banks can increase lending when they have enough liquidity, and one of the biggest sources of liquidity is the government. There is a need to ensure liquidity is getting transferred to the banks,” said Nsekela.

“The best way of lowering interest [and encouraging more lending] is to innovate in lending by creating incentives that will allow for lowering interest,” he suggested.