The Ministry of Minerals informed the parliament in April 2026 that the Tanzania Extractive Industries Transparency Initiative (TEITI) had disclosed information about three mining contracts during the past year, and added that TEITI would “continue to disclose contracts” entered into between the government and mining companies.

To set the record straight, TEITI has not disclosed contracts but basic information, or summaries, about three contracts. Moreover, the published information does not meet the standard set by the Extractive Industries Transparency Initiative (EITI), despite the Ministry’s claim that the disclosure is in compliance with the 2023 EITI standard.

The 2023 EITI standard, the latest, requires member countries to disclose full texts of contracts and disallows summaries or excessive and unnecessary redaction. Our research confirms that TEITI has, during the past year, published three summaries which it describes as “framework agreements.”

However, the three documents completely fit the definition of what EITI does not regard as sufficient to meet contract disclosure requirements. Besides, it’s hard to see how any of those documents advances the course of accountability in the country.

Tanzania joined EITI in 2009, a period when public concerns about unfair mining contracts and corrupt practices were notably high. As a global initiative, EITI originates from the idea that opaque extractive governance encourages corruption and precludes accountability. In contrast, transparency along the entire extractives value chain facilitates civil society oversight and strengthens intra-governmental checks and balances.

Costly reform

Six years after joining the EITI initiative, the parliament of Tanzania debated and passed the Extractive Industries (Transparency and Accountability) Act (CAP 447) to address the sector’s problematic opacity. Although significant, it was a step too late.

READ MORE: Weak Oversight Threatens Tanzania’s LNG Potential

More than two decades of suspicion and unaddressed concerns culminated in President John Magufuli’s decision to overhaul the sector in 2017, although at a huge cost for both the public and the industry. Firms that disputed invitations to renegotiate their concessions or felt aggrieved by cancellations fought back through arbitration and litigation.

In settling the claims, Tanzania lost about US$150m in direct payments (see table 1). Much more must have been lost in arbitration appearances overseas and shuttle diplomacy to resolve cases of seized assets.

Table 1: Settled arbitration cases (2020 – 2025)

| Arbitration case | Duration | Claim and manner of resolution | Details | Amount paid (on settlement) |

| Winshear Gold Ltd | 2020-2023 | Claim not clear. Settled by the parties. | Cancellation of four mineral exploration retention licences in South Western Tanzania. | US$30 million |

| Indiana Resources Ltd | 2020-2024 | US$76.7m claimed. Settled by the parties. | Cancellation of retention licence for Ntaka Hill Nickel project in Southern Tanzania. | US$90 million |

| Montero Mining and Exploration Ltd | 2021-2024 | US$70m claimed. Settled by the parties. | Cancellation of Wigu Hill rare earth licence. | US$27 million |

The 2017 reform efforts led to the adoption of stringent resource sovereignty laws that, unexpectedly, acknowledged the occasional need for parliamentary review of contracts. Section 12 of the Natural Wealth and Resources (Permanent Sovereignty) Act of 2017 provides that “all arrangements or agreements entailing extraction, exploitation or acquisition and use of natural wealth and resources may be reviewed by the National Assembly.” As you might imagine, the use of ‘may’ made parliamentary review optional and the clause useless.

Although aggressive and contested, Magufuli’s actions triggered a good deal of introspection. The Chief Executive Officer of Acacia, now a defunct company, acknowledged something that Tanzanians had long known: that international mining companies had secured terms that were legal but not necessarily just and “not equitable.” Decades of contractual secrecy allowed the likes of Acacia, their beneficial owners, and a few Tanzanian elites to reap undue benefits without any meaningful scrutiny or accountability.

Cosmetic disclosure

Since the adoption of the extractives transparency and accountability law in 2015, transparency in the extractives sector has become a question of whether Tanzania is complying with its own legal requirements or not. In terms of contract disclosure, a short and clear answer is no. All regimes that have held office since the inception of industrial-scale mining in Tanzania have been reluctant to disclose mining contracts.

READ MORE: Tanzania: Assessing and Mitigating Political Risks for Businesses Post–October 29

As indicated earlier in this article, we examined the three summaries that the Ministry of Minerals takes credit for publishing. All three appear to have been signed in December 2021; the first being between the Government of Tanzania and Mahenge Resources Limited, while the second summary relates to a contract between the Government of Tanzania and LZ Nickel, a company which owns interests in the Kabanga Nickel concession.

The third summary focuses on the Mwadui Diamond Mine. All three documents appear to have been posted on the TEITI website on May 4, 2025, a year late given that TEITI’s own disclosure plan had identified May 2024 as the intended publication date.

The three summaries lack meaningful commercial terms and fail to reveal public stake in concessions held through subsidiary firms. For example, the Tembo Nickel concession, which is a joint venture between the Government of Tanzania and Kabanga Nickel Limited, has subsidiary arrangements for investments in refinery capacity but lacks clarity on government ownership.

Moreover, the summaries do not reflect the latest ownership arrangements. As an example, the reported acquisition of Petra Diamond shares in Mwadui mine by Caspian Limited is not captured by the respective summary.

Although shallow, the summaries reveal important legal contradictions. The summary about Kabanga Nickel indicates the contract with the Tanzanian government is governed by Tanzanian law but is subject to international commercial law (UNCITRAL) for dispute resolution purposes.

The terms of the other two concessions relating to Mwadui diamond and Mahenge graphite are governed exclusively by Tanzanian law, although all three concessions were seemingly signed during the same time. This variation underscores the reality that Tanzania is still struggling to avoid international arbitration, a practice restricted by its 2017 natural resource sovereignty laws.

READ MORE: To Get the LNG Project Right, Avoid Mistakes Made in Mining

With Tanzania expected to sign a Host Government Agreement (HGA) for the prospective Liquefied Natural Gas (LNG) project in Southern Tanzania in the near future, and likely to see a Final Investment Decision (FID) for the Kabanga Nickel project during the same period, the issue of extractive sector transparency cannot be more relevant.

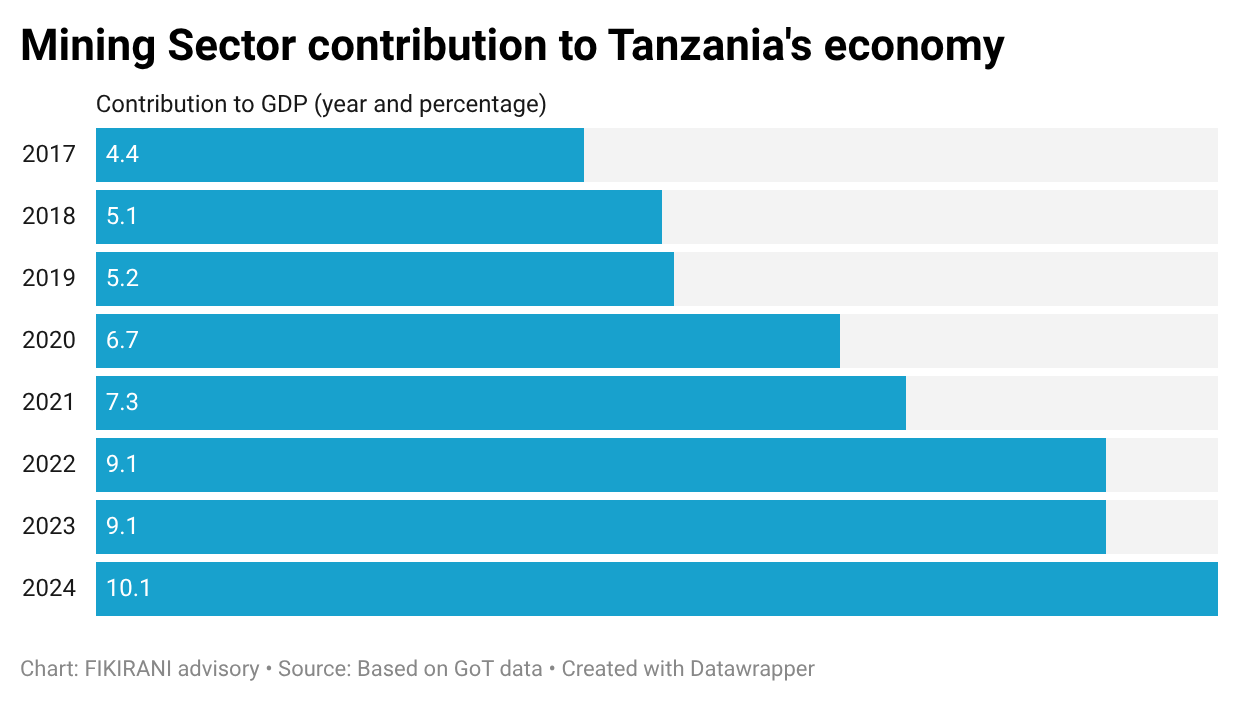

After all, Tanzania’s extractives sector is booming again, after contracting during the chaotic 2017-2019 reform period. Based on recent government of Tanzania data, the mining sector alone exceeded 10 per cent contribution to the country’s economy in 2024. Unfortunately, even as Tanzania’s extractives sector has expanded, civil society oversight of the industry has weakened.

Weak civil society oversight

Civil society oversight of the extractives sector has weakened, from its pinnacle in the 2008-2010 reform period, to its current lowest posture, thanks to the unprecedented narrowing of the civic space and severe funding constraints. Even the EITI, which is not known for being vocal on civic space, placed Tanzania on “enhanced monitoring” after last year’s electoral violence.

On funding, Western nations have radically reduced foreign aid even as their appetite for energy and critical minerals has skyrocketed. Preliminary estimates by the Organisation for Economic Cooperation and Development (OECD) point to a 23.1 per cent decline in overall Official Development Assistance in 2025.

Our research finds that the national coalition of organisations working on extractives, HakiRasilimali, has seen a significant decline in the share of its active members due to years of dwindling resources.

To its credit, the government of Tanzania has strengthened the TEITI secretariat by hiring an Executive Secretary and improving the staffing of various departments. However, as a quasi-governmental institution, TEITI remains fundamentally constrained by its lack of independence.

Although viewed within the government as an “advocacy” entity (taasisi ya kuhamasisha uwazi), TEITI is not able to engage in the sort of advocacy carried out by civil society. And given the challenges afflicting civil society, TEITI reports have become a performative tool; published largely for compliance reasons.

So, who benefits?

The primary beneficiaries of the veil of secrecy that hangs over the Tanzanian extractives sector are the corporate entities that exploit the country’s natural resource wealth. Secrecy implies less scrutiny and little accountability.

Some of these corporate entities have complained about participation in EITI and cited duplication as the main reason due to the requirement to also report to the Business Registration and Licensing Agency (BRELA) and the Tanzanian Treasury.

While there is indeed a need to streamline reporting, transparency in the extractives sector became a legal requirement when Tanzania adopted a specific law in 2015. Unfortunately, the accountability chain is broken and could stay this way for the foreseeable future.

Dastan Kweka is a researcher and analyst based in Dar es Salaam. He is available at kwekad@gmail.com and on X as @KwekaKweka. The opinions expressed here are the writer’s own and do not necessarily reflect those of The Chanzo. If you are interested in publishing in this space, please contact our editors at editor@thechanzo.com.